En español, en français, em português.

Following several months of adaptation, on the 19th of January Google began to roll out changes it made in order to comply with DMA (Digital Markets Act) requirements; a roll-out that finished on the 7th of March.

Just days after the first changes were implemented, we began to see how they influenced hotel campaigns in Google Hotel Ads. Three months on, results for hotels are still getting worse:

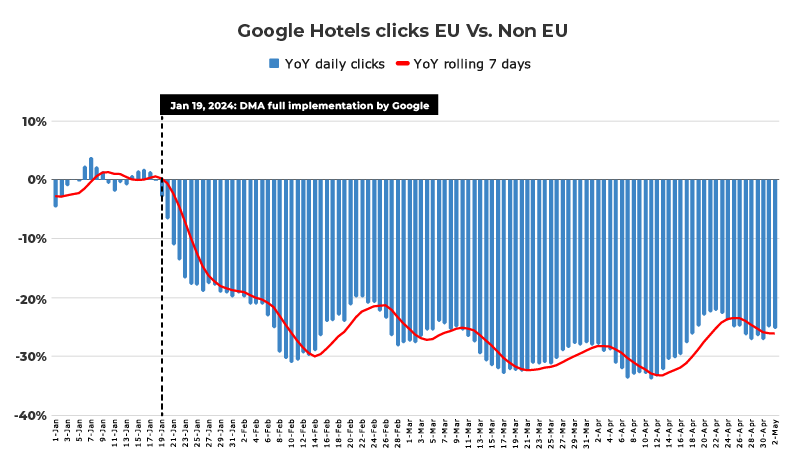

- Just over three months following implementation, click-through data has shown a 30% decrease in traffic volume in EU markets affected by DMA implementation compared to those markets where DMA has not been implemented.

- The graph below shows the Google Hotel Ads click differential between regions affected by the DMA vs. those not affected, revealing a click volume drop of 30%.

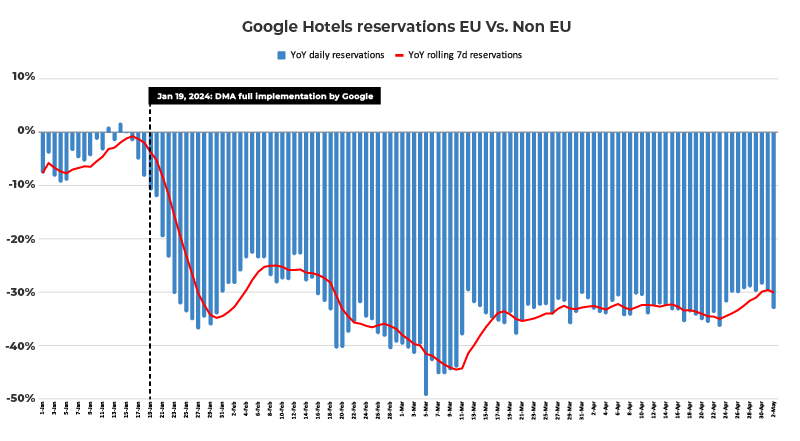

- The volume of direct bookings drops as much as 36%, increasing hotel dependence on intermediaries, which seriously damages their profitability.

What has changed exactly?

Basically, Google has been obliged to alter its results scheme for travel searches (flights and hotels).

Here we will focus only on changes that have affected hotels.

BEFORE (and currently in non-DMA markets):

NOW (implemented in DMA markets):

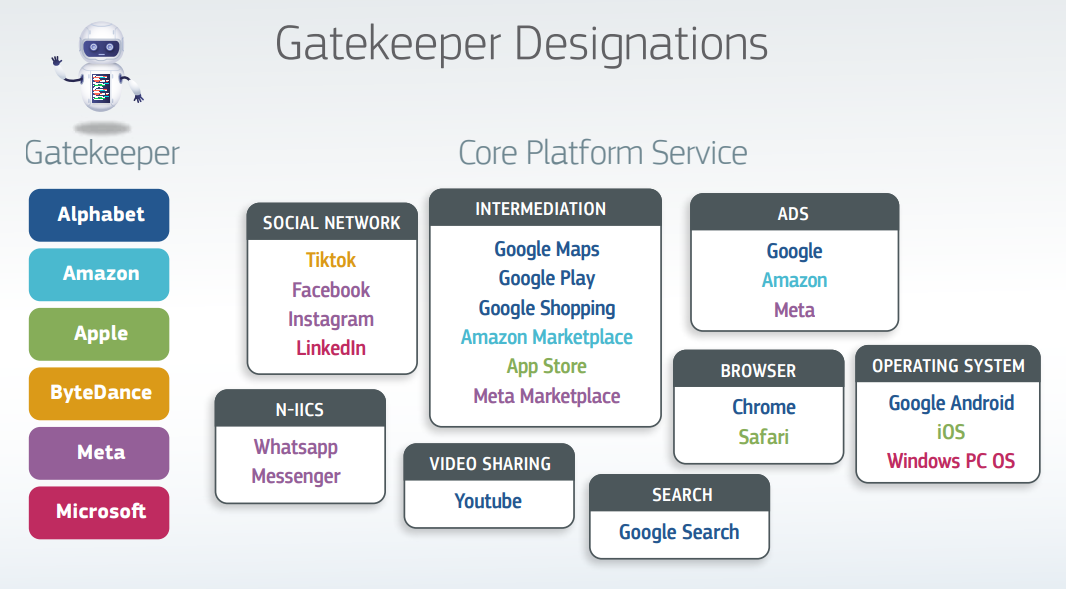

In July 2023, the European Union designated six digital companies as gatekeepers, Amazon, Apple, ByteDance (TikTok), Alphabet (Google), Meta (Facebook) and Microsoft (Windows), on the basis of the relevance of the 22 platforms operated by these companies.

In the case of Google, the gatekeeper designation means it cannot include its own vertical services (Google Maps, Google Flights or Google Hotel Ads) in its search results pages (known as SERPs). The specific article in question is Article 6.5 of the DMA, which deals with ‘self-preferencing’.

Verbatim extraction from the DMA:

“The gatekeeper shall not treat more favourably, in ranking and related indexing and crawling, services and products offered by the gatekeeper itself than similar services or products of a third party. The gatekeeper shall apply transparent, fair and non-discriminatory conditions to such ranking“.

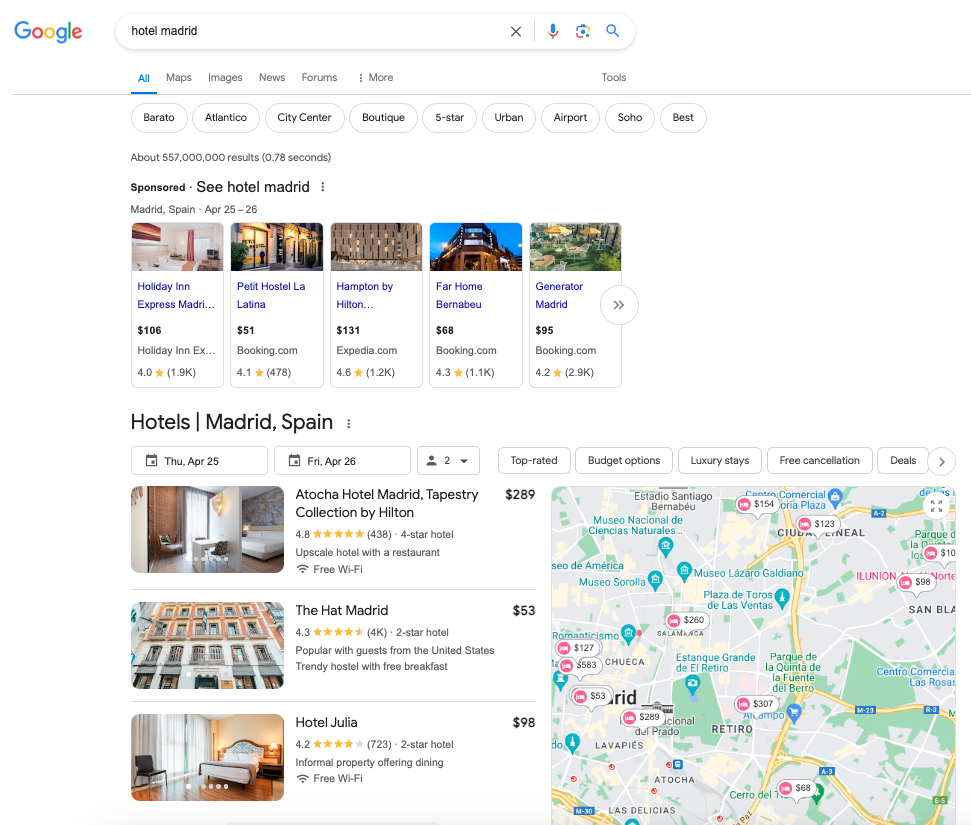

This means that presentation of hotel offers to users based in DMA markets is less organised, clear and intuitive.

Prior to DMA, Google’s taxonomy of results was the result of decades of effort by the company to refine its results in order to provide an optimized search experience that would connect supply and demand in a way that was ideal for both.

This pre-DMA search experience offered hotels participating directly in the Google Hotel Ads product, the option to present their inventory (availability and room rates) in a way that was both efficient from the standpoint of distribution cost, and enriched for the user, as it integrated the experience of other services, e.g. Google Maps. This way of presenting information was clear, relevant and intuitive, and maximized purchasing decisions such hotel bookings for those users who were so inclined.

What has been lost with the implementation of the DMA?

From the user perspective

The user can no longer:

- View the hotel offer at the destination (availability and prices in aggregate(.

- Click on the Google Maps link to locate the hotel. This point is particularly frustrating.

- View the ‘hotel package’ (selection of three hotels with availability, price and user ratings) in which both hotels with websites and intermediaries could participate.

- Change the dates and other booking elements, such as the number of travellers per room (these are updated in the search engine and not in the hotel file), in an easy, user-friendly way during the booking process.

- View calendar prices.

- Easily access the Google Travel environment for more comprehensive travel information.

- Clicking on ‘Book a room’ opens search engine results, rather than the Travel section.

- Instead of clicking on the price, the user must click on ‘Visit Site’.

- All interactions with the form modify the search engine results (SERP).

From the hotel perspective

The hotel has lost visibility in terms of the user experience, which can be proven as follows:

- 30% drop in clicks to websites in markets affected by DMA.

- 36% drop in direct bookings in markets affected by DMA.

Source: Mirai. Traffic volume comparison of 3450 hotels between DMA and non-DMA markets from 01.01.24 to 22.04.24

While we cannot affirm the fate of these ‘lost clicks’, given that existing demand is a ‘zero-sum game’, the most plausible hypothesis is that the difference in clicks in DMA markets is being captured by those advertisers that have gained visibility and prominence in the new results format, these being intermediaries such as OTAs (Booking.com and Expedia, mainly).

And Booking.com… is it not a gatekeeper?

In the context described above, this is the key question, the answer being ‘not at the moment’.

Update May 13, 2024: the European Commission ratified Booking.com as gatekeeper. On November 13, 2024 the EU will notify Booking.com of changes to be made to its platform.

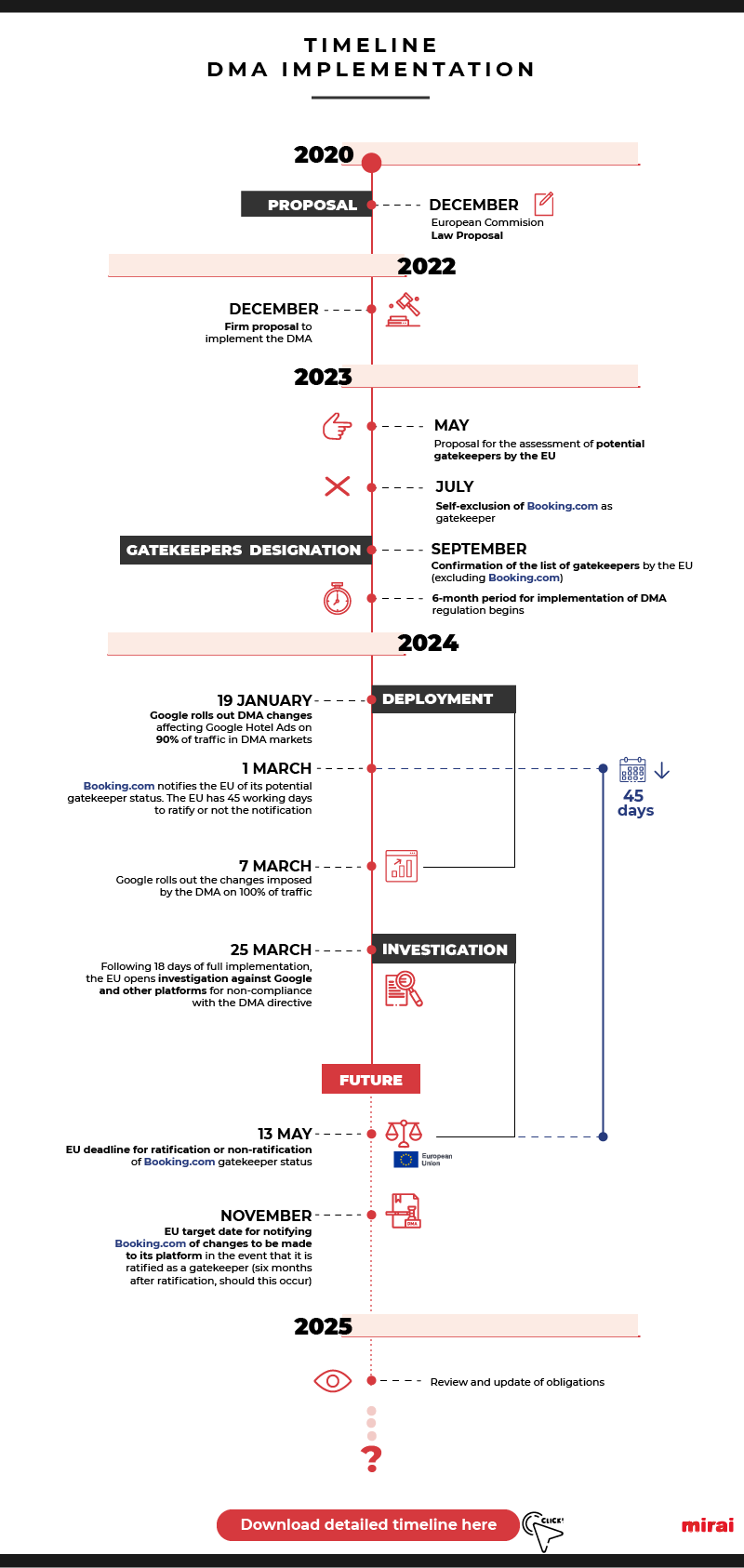

In the following graph we take a closer look at how the events unfolded:

Let’s look at the sequence:

- December 2022:

– Firm proposal to implement the DMA.

- May 2023:

– Proposal for the assessment of potential gatekeepers by the EU.

- July 2023:

-Self-exclusion of Booking.com as gatekeeper.

- September 2023:

– Confirmation of the list of gatekeepers by the EU (excluding Booking.com).

– 6-month period for implementation of DMA regulation begins.

- January 2024:

– 19/01/24: Google rolls out DMA changes affecting Google Hotel Ads on 90% of traffic in DMA markets.

- March 2024:

– 01/03/2024: Booking notifies the EU of its potential gatekeeper status. The EU has 45 working days to ratify or not the notification.

– 07/03/2024: Google rolls out the changes imposed by the DMA on 100% of traffic.

– 25/03/2024: Following 18 days of full implementation, the EU opens investigation against Google and other platforms for non-compliance with the DMA directive.

- May 2024:

– 13/05/2024: EU deadline for ratification or non-ratification of Booking.com’s gatekeeper status.

- November 2024:

– 13/11/2024: EU target date for notifying Booking.com of changes to be made to its platform in the event that it is ratified as a gatekeeper (six months after ratification, should this occur).

What does this mean for the hotel industry?

The key result of the implementation of the DMA for hotels is that they have lost visibility in the markets affected by the DMA, and as such they have lost direct sales capacity, their profitability has been reduced and their dependence on intermediaries increased.

The EU, in its efforts to make the DMA a fairer, more balanced market, is obliging gatekeepers to adapt to the regulation. As a result, these changes are subjecting hotels to the toll of intermediation, strangling direct sales and holding users and hotels captive to less profitable, less independent business models.

If Booking.com is ratified as gatekeeper, it remains to be seen what measures are imposed and the consequent degree of compliance. In any event, assuming they were restrictive and favourable to the hotel industry, Booking.com would have gained more than a year’s competitive advantage by enjoying the increased visibility afforded by the changes imposed by the DMA since January 2024.

Who stands to gain from all this?

In theory, the user should be the primary beneficiary of implementation of the DMA.

Today, the user experience on the Google hotel search results page is less clear, less intuitive and requires a higher number of clicks, thus ‘pushing’ the user to purchase through intermediaries a service that previously could be purchased directly from the producer with greater clarity, ease, competitiveness and efficiency for all concerned.

We should not forget that, in the event an in-house marketing strategy exists (a transactional website allowing booking), the best source for a service/product is always the producer, assuming the service/product is marketed properly and coherently.

OTAs, in particular Booking.com, due to its presence and relevance in Europe, are gaining even more visibility and prominence in Google search results since the DMA has been rolled out. It is difficult to determine precisely, but a substantial part – if not all – of the 30% of clicks lost by hotels are going to intermediaries.

Will the EU impose some kind of equivalent restriction or change of practice on Booking.com?

It is difficult to anticipate what will happen. The EU has to date taken an asymmetrical approach to the interpretation of its own rules by excluding Booking.com from the first group of designated gatekeepers.

If it finally ratifies Booking.com as gatekeeper and imposes some kind of limitation on it, this will be at the end of 2024. As we cannot know the decision or its scope, the only certainty we have is that Booking.com will have enjoyed at least eleven months competitive advantage as a result of the EU’s erratic application of the DMA.

The remaining intermediaries (Expedia and others) could continue to enjoy the competitive advantage derived from non-gatekeeper status forever.

It is worth noting that the EU’s current implementation of the DMA favours large US companies, such as Booking Holdings or Expedia, while harming the European user experience by reducing the profitability and competitiveness of the hotel ecosystem, especially for smaller independent chains and hotels.

At Mirai we have been actively involved since 2022, working directly with the EU, Google and the European hotel industry in an effort to ensure that implementation of the DMA is beneficial for the entire European hotel ecosystem.